Today, the services at approximately 80,000 bank branches across India came to a standstill as employees of public sector banks (PSBs) observed a one-day strike. This protest was directed against the ongoing consolidation efforts by the government, which aim to merge several public sector banks into fewer, larger entities. The strike brought attention to a critical issue that has been a recurring theme in India’s banking sector for decades.

A Brief History of Bank Mergers

The consolidation of banks is not a new concept in India. In the 1990s, there were discussions about the benefits of merging large and small banks. A notable instance was the merger of the New Bank of India with Punjab National Bank (PNB) on September 4, 1993. Having been closely involved in this merger at PNB’s Head Office, I witnessed the intricate processes of finalizing accounts and getting them audited by statutory auditors. This experience provided a firsthand understanding of the complexities and challenges involved in bank mergers.

Recent Developments in Consolidation

After a long hiatus, the government has once again brought the issue of PSB consolidation to the forefront. In a significant move, Finance Minister Arun Jaitley announced a roadmap for consolidation in his budget speech, followed by the establishment of an expert panel to explore this further. The government’s ultimate goal is to reduce the number of PSBs from the current 27 to about 8-10. A major step in this direction was the union cabinet’s approval on June 15 to merge the five associate banks of State Bank of India (SBI) with the parent bank.

The Rationale Behind Consolidation

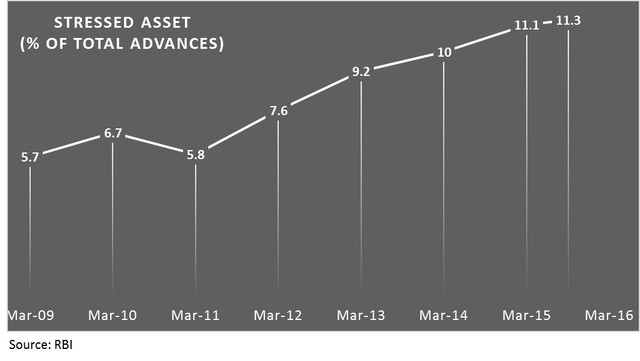

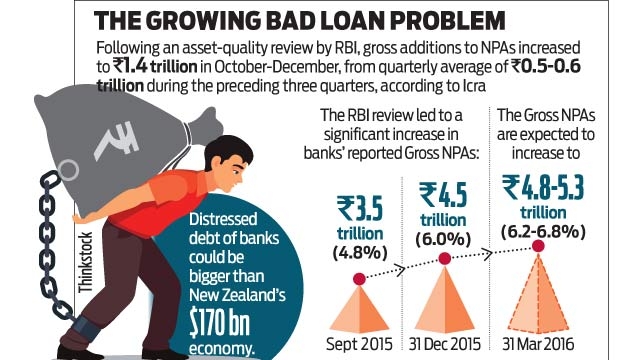

The push for consolidation is part of a broader strategy to reform the banking sector. The idea is to create larger, more robust banks that can compete globally and manage larger economic activities. However, the timing of these mergers is critical. Currently, Indian banks are grappling with stressed assets, which have reached alarming levels. Gross non-performing assets (GNPA) and restructured assets (RA) among PSBs are approximately 112% of their equity, amounting to INR 5.9 trillion (USD 88 billion) as of March 31. This has put immense pressure on banks’ balance sheets and capitalisation levels.

Challenges with Stressed Assets

The surge in stressed assets can be attributed to several factors, including high corporate leverage and aggressive lending to the industrial sector between 2005 and 2011. This period saw an average lending rate of over 20%, despite the well-known risks of high leverage. Consequently, banks are now dealing with significant non-performing assets (NPAs), which require substantial provisioning and impact profitability.

Concerns and Opposition

Moody’s Investors Service has highlighted the risks associated with consolidating PSBs in the current weak economic environment. While consolidation could potentially strengthen bargaining power, reduce costs, and improve governance, the immediate risks are considerable. Many PSBs are struggling to meet regulatory capital requirements and are trading at significant discounts to their book value. This financial strain makes it challenging for any PSB to take on the role of a consolidator without risking its own stability.

Moreover, government support in the form of equity capital is essential for successful mergers. Employee unions also pose a significant challenge, as their opposition can increase merger costs and complicate integration efforts. For instance, SBI’s merger with its associate banks is estimated to cost up to INR 30 million (USD 0.45 million) due to differences in employee pension schemes.

The Path Forward

While the concept of having a few large banks to achieve scale and synergy is logical, mergers alone will not improve asset quality immediately. The capital requirement for these banks will remain, and various factors such as trade unions, technology, business models, and human resources need to be considered. The critical question is whether these mergers will occur under distress or as part of a strategic, well-planned process.

In conclusion, while today’s strike by PSB employees highlights the immediate resistance to consolidation, it also underscores the need for a carefully considered approach to reforming India’s banking sector. The government must balance the long-term benefits of consolidation with the short-term challenges to ensure a robust and resilient banking system.

& is it the only solution?

Definitely not under a distress situation or in a highhanded manner.

how they propose to fund & how long ? No mention of this anywhere .

Where’re the funds needed for banks? Big, sound banks should be allowed to go to public. Government better go for effective regulation. For weaker banks, Government may bring back recapitalisation bonds as it had done it in 1990s, with a minimum effect on budget and revenue deficit.

The mounting bad debts is a matter of grave concern as rightly highlighted by you. Also, financial constraints and incompatibility between banks may be a serious threat that really requires key strategizing and commitment. Looks like there is a certain pattern and cycle to merger and then again going separate ways..

Hope with the passing of the Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill today by Lok Sabha along with the Insolvency and Bankruptcy Code passed in May, there will be some faster recoveries and improvements in bad debt situation.

High bad debts not only raise the borrowing costs but also impact in credit delivery.

Sir, as you have pointed out If the merger costs outweigh the synergies gained, the benefits will be hard to accrue, at least in the short term. Also how will the merger improve the existing non performing assets, On one hand it is easier to implement good governance framework, and have reduced cost of operations post consolidation, on the other hand the banks may become too big and maybe unapproachable for small borrowers.

Your apprehensions are quite justified. As the banks grow in size their products/ service level also change. India do need some mega banks to finance the big projects, infrastructure financing, large ticket trade finance, but that doesn’t mean that there’s no scope for small banks. RBI is giving licenses to small banks and payment banks to serve the unbanked areas, primarily. We need to balance our plan with our need and grow. It cannot be a single dimensional trajectory. You can see in the US they have community banks, credit unions running side by side JPMorgan or Citibank. Also, technology is a big enabler. We are getting some new fintech startups doing good business and they too have an excellent future, if regulated prudently.

Yes a right mix is required.

Presently the financing of infrastructure projects is mostly done by a consortium of lenders, which distributes the risk as well. Sir want to understand how it helps if instead of a consortium the projects are financed by a single lender?

The idea is not to change from a consortium of banks to a single bank, not to concentrate the risk at one place. Larger size of the banks give better bargaining power in the hands of the banks for effective monitoring of the assets/business lent.

With the increased requirement of capital to meet the latest Basel III requirements, banks need to raise capital to be able to finance and be on operation. Every loan is a risk. There is a limit to which a bank can take on risk, which is guided by Capital Adequacy Ratio, Leverage Ratio etc. More the capital, more is the risk taking ability of the bank.

Good banks can subsidise the capital requirement of a bad bank if the bad bank is merged to it. This will ease the pressure on government to recapitalise the PSU banks.

Again very large size comes with different issues. All systemically important banks have to maintain additional capital, higher than other banks so as to avoid “too big to fail” situation.

Consolidation improves efficiency, increases synergy, rationalises branch networks, boosts competitiveness. However, a merger should not be done under a distress situation or in a highhanded manner.

I see..easing the pressure for recapitalisation of PSU banks is a key factor in favour of consolidation.