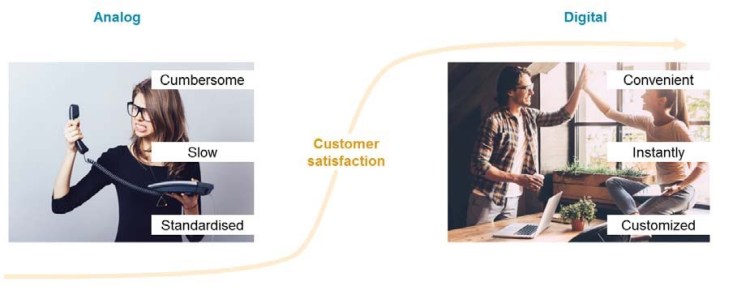

In the ever-evolving landscape of the digital age, established organizations find themselves at a critical juncture. The allure of new opportunities beckons, yet the challenges loom large. Customers today demand immediacy, convenience, and customization in their services. If a better offer presents itself online, loyalty becomes a fleeting concept, as customers readily switch allegiance.

Over the past decade, industries have undergone seismic shifts in their value propositions. Traditional multinationals once held sway, but the emergence of responsive, scalable digital entrants has reshaped market dynamics. This shift, often termed disruption, is not merely a threat but a golden opportunity to reinvent value creation through the adoption of new-age digital principles.

Nowhere is this more evident than in the financial sector. Banks worldwide are amidst an era of hyper-digitization, where the traditional modus operandi is being upended by disruptive forces from various quarters. The advent of new entrants poses a significant threat to incumbent banks, urging them to adapt or risk becoming obsolete.

Disruption in the financial services sector is posing formidable challenges for incumbents. This is largely due to the various products and services new players offer that incumbents are still getting accustomed to and trying to adapt. A digital attacker is one that typically has no physical locations and serves its customer primarily through digital platforms.

Digital attackers — that is, digital-only banks using a cloud-native, low-cost platform — historically were secondary banks for consumers. Many attackers garnered smaller deposits and more limited lending than traditional banks. Incumbent banks need to watch out for these digital attackers because not only do they serve as an alternative to banks, they are also leaders in adopting technology, helping customers and businesses to uproot legacy technology that plagues traditional players.

Digital attackers have gained ground among consumers, and they hold more promise than initially meets the eye. Traditional banks risk losing market share if they don’t respond to these new models. An inflection point in adoption is near, as some attackers have shown that they can please customers and achieve a large scale. They are expanding from retail to small business accounts, from deposits and basic transactions to lending.

With innovative opportunities and leadership commitment, digital attackers can embrace challenger ambitions in line with global leaders. Key initiatives include enabling secure data exchange, embedding third parties on the bank’s platform, originating and/or embedding bank products on third-party platforms, supporting the launch of micro-banks and providing customers with third-party apps.

For traditional banks, the rise of digital attackers signals a call to action. Failure to respond effectively could result in a loss of market share and relevance. The trajectory of digital attackers, from retail to small business accounts, from basic transactions to lending, underscores their potential to reshape the industry landscape.

Many incumbent banks have realized the compelling logic of having a separate digital bank. Regulatory changes (such as open banking initiatives and the Revised Payment Services Directive, PSD2, in the European Union, or video-KYC and Unified Payments Interface in India) that are designed to promote innovation, better prices and a better experience have primed the field for more competition.

We are seeing the major private sector banks in India such as Kotak Mahindra Bank, HDFC Bank, Axis Bank, DBS Bank, etc. offering digital saving products, which give the consumer the luxury of freely accessing and performing their traditional banking activities 24×7 without having to personally go to a bank branch to get their work done. Digital banking can be done either through a laptop, a tablet or a smartphone. This is just the beginning and the future will show many incumbent banks adopting the agility and customization of the digital attackers.

At the current rate that digital attackers are progressing and evolving, traditional financial services firms will need to learn to disrupt, or they will be disrupted. Incumbents can gradually move toward a challenger model by swiftly adding new digital capabilities on top of their current model.

Yet, this is just the beginning. The pace of digital disruption shows no signs of slowing down. Traditional banks must adapt swiftly, incorporating digital capabilities into their existing framework, lest they fall behind.

Yes, the banking industry is going through an upheaval.

Thanks, Grover sir.

Good view on the banking future.

Thanks, Sanchita.

The most unfortunate part of digital banks is accessibility. The only way these are accessible is with a toll-free number. The most frustrating part is the experience with the toll-free number. Many banks have restricted dial-in with preset numbers and often the problem we face is not configured in such a set-up. Paytm is one such example. In stark contrast, the new small banks offer excellent services.

True. But with chatbox, robotics, AI, etc. things are getting smoother. Every bank needs to be agile and evolve continuously to remain in competition.

I hope so. Many of the systems that banks employ are not designed to delight the customers. The banks need to be proactive else they will lose customers to the one that are more sensitive to their needs. Let’s hope it paves way for better banking infrastructure.

Yes, sure. Technology cannot replace the human touch in service delivery but can definitely enhance the user experience if deployed properly.

truly!

Very informative indeed. May be good security practice like strong password etc is required.

Thanks, Mano. Along with a ribust digital infrastructure, we need to develop a sound digital culture to prevent innocent citizens from being looted. Digital and financial literacy is a must to survive in the coming days.